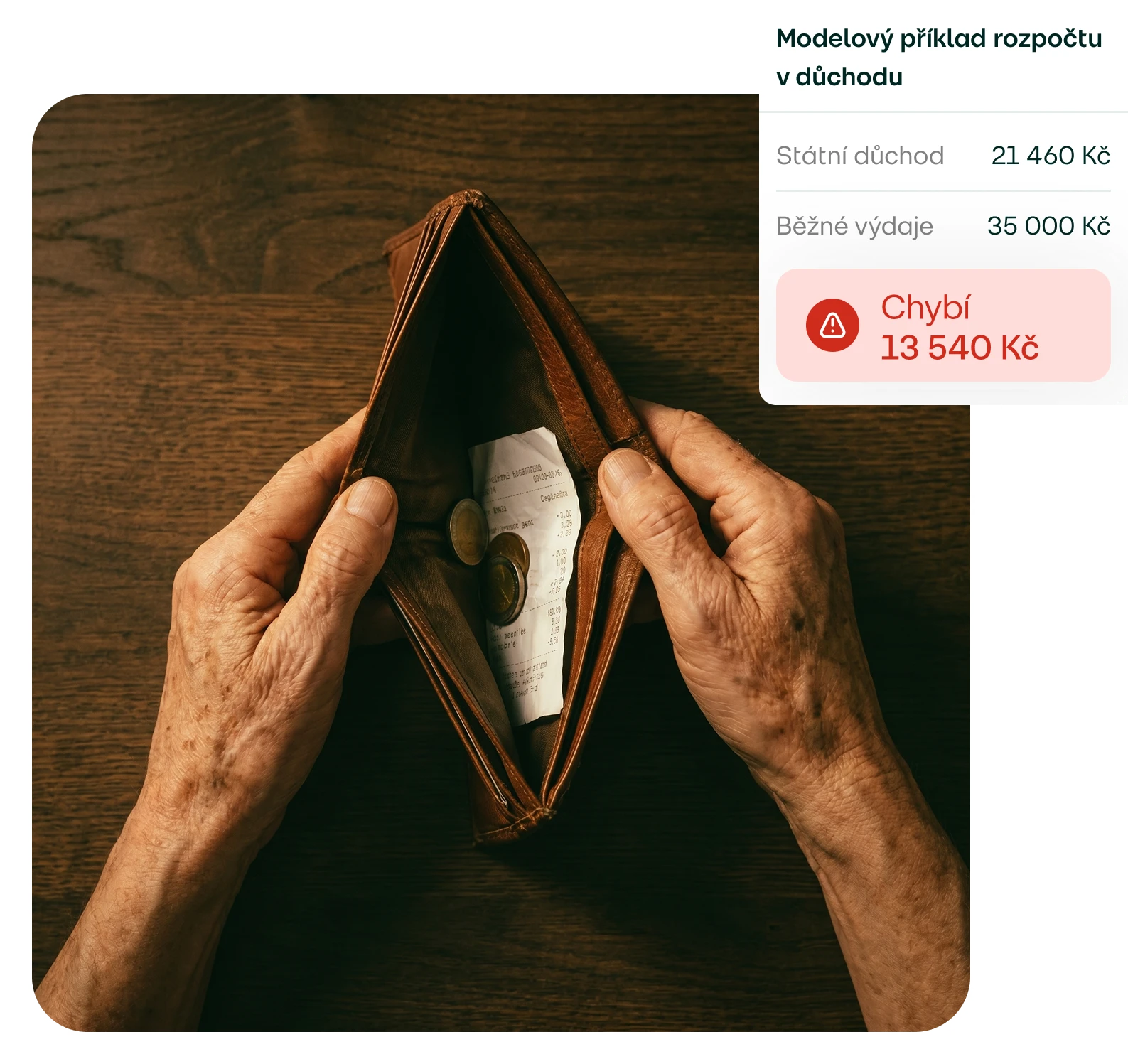

Most people know this. Yet they keep putting off planning for retirement. The earlier you start, the less you need to set aside to maintain the lifestyle you want in retirement.

Illustrative example; actual amounts vary by income and legislation.

The Long-term Investment Product (DIP) combines long-term investing with state tax support. You build your own retirement reserve and can deduct part of your invested money from your taxes every year.

Regulated by the CNB

We are a licensed securities dealer regulated by the Czech National Bank.

Tax savings

You can deduct part of your contributions from your tax base each year.

Lower fee

A lower fee means more of your money keeps working for you.

We’ll help you invest

Getting started is easier than you think

1.

Tell us your goals

A short questionnaire helps us understand what you expect from investing.

2.

We’ll propose your investments

Based on your answers, we’ll present investments that match your needs.

3.

Put your money to work

Make your first deposit, we’ll buy your investments and take care of them going forward.

Důchodová kalkulačka

Calculate your second pension.

Find out how much you’ll save, or how much to invest each month to reach the income you want. We calculate the DIP tax saving right alongside.

Recommended monthly investment

3 098 CZK/mo.

To receive 30 000 CZK per month in retirement.

Total savings

7 200 000 CZK

Total tax saving

+167 287 CZK

What do you want to calculate?

Switch between finding out your total savings or how much to invest for your desired monthly income.

We calculate with an expected annual return of 10.13 % p.a. and pension payout over 20 years.

Recommended monthly investment

3 098 CZK/mo.

To receive 30 000 CZK per month in retirement.

Total savings

7 200 000 CZK

Total tax saving

+167 287 CZK

The calculator uses a model example for illustrative purposes. The return shown is based on the historical performance of the Audacious portfolio 10.13% p.a. Historical performance is calculated as the average annual return over 10 years to 1 June 2026 in euros, based on a simulated historical development using the prices of individual ETFs or their underlying indices. The return is calculated before fees. Investment value may fluctuate and past returns are not a guarantee of future returns. The simulation does not account for tax implications or inflation. Investing involves the risk of losing part or all of the invested amount.

Your investment

The Long-term Investment Product (DIP) works on the same principle as our other accounts. You invest in a broadly diversified ETF portfolio with full transparency.

Annual tax saving

You can deduct part of your contributions from your tax base each year.

More money stays with you

A lower fee means a larger portion of your investment keeps compounding.

Standard or ESG option

You can choose between standard and sustainable investing.

Better than a pension fund

Lower fees, higher potential returns, more control.

Your investments, in your name

Held in your name and kept separate from Direct Fondee’s assets.

Flexible payout

Once conditions are met, you can take your money all at once, in stages, or as a regular income.

Annual tax saving

You can deduct part of your contributions from your tax base each year.

More money stays with you

A lower fee means a larger portion of your investment keeps compounding.

Standard or ESG option

You can choose between standard and sustainable investing.

Better than a pension fund

Lower fees, higher potential returns, more control.

Your investments, in your name

Held in your name and kept separate from Direct Fondee’s assets.

Flexible payout

Once conditions are met, you can take your money all at once, in stages, or as a regular income.

THE MORNING YOU’RE LOOKING FORWARD TO

Retirement isn’t just about money. It’s about the freedom your money gives you when you no longer want to work full time.

Greater peace of mind

In retirement, you won’t have to count every penny.

Time for your plans

For travel, family, hobbies - or whatever brings you joy.

A benefit from day one

You’re saving for the long term, but you can benefit from the tax saving every year.

Who can open an account

You can open a pension investment account from the age of 18. At Fondee you can have one pension portfolio, designated for investing within the Long-term Investment Product (DIP).

When you can withdraw

To keep all DIP benefits, you can withdraw penalty-free from the age of 60, and only after at least 10 years from account opening. You can choose to receive the full amount at once or withdraw gradually.

Tax benefits and employer contributions

Your employer can contribute to your DIP, similarly to a pension savings plan. You can also deduct your own contributions from your tax base under the current DIP rules.

If you want to withdraw early

You can close your pension account at any time, even before meeting the DIP conditions. In that case, you lose the associated benefits - particularly tax relief, which you’ll need to repay. We’ll also recalculate the difference between the discounted and standard fee.